A few years right back, Federal national mortgage association as well as brother financial Freddie Mac circulated mortgage programs called HomeReady and you will House You can easily, respectively. Its mission? To take on the three.5% down FHA financing system that assist lower- in order to modest-earnings individuals buy a property without a lot of bucks.

However, investors that simply don’t notice residing in the house or property for a beneficial year can also enjoy step three-5% down mortgage apps out-of Fannie, Freddie, together with FHA.

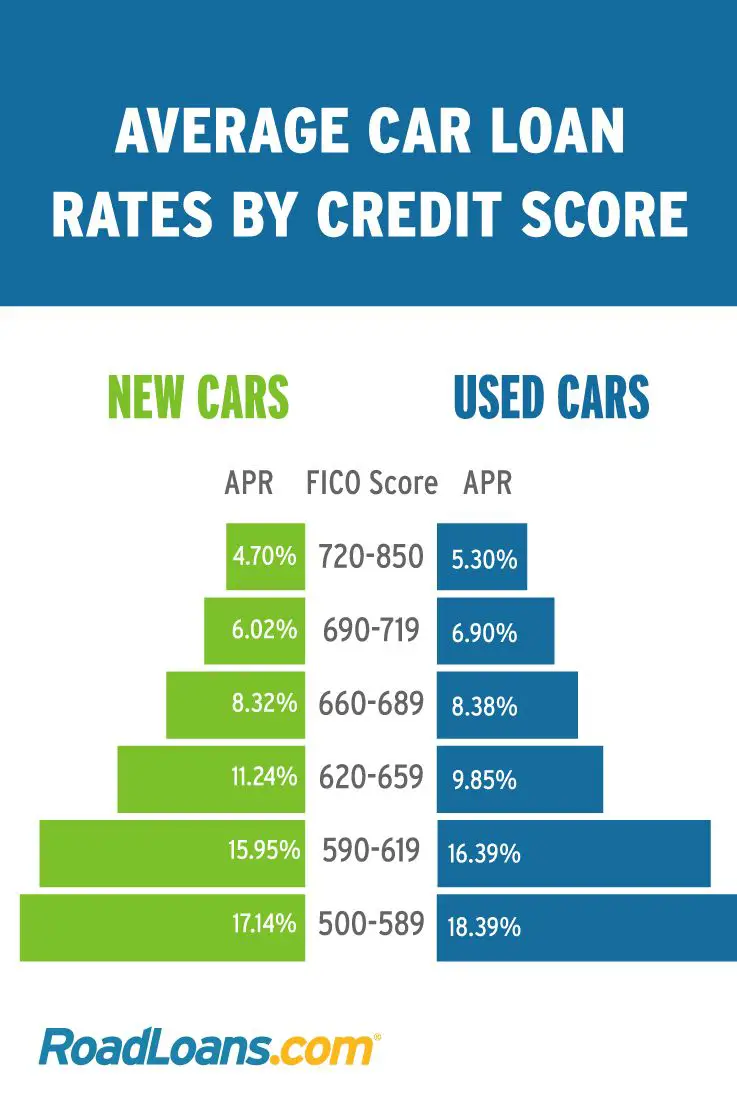

Trick Takeaways:

![]()

- Buyers can obtain single-friends belongings that have step three% off and two-to-four-device land that have 5% off, however, have to are now living in the home for at least one year.

- Immediately after 12 months, they may be able escape and keep maintaining the home given that a non-owner-occupied local rental property.

- You can utilize the future rents from other devices to simply help you be eligible for the borrowed funds.

Fannie mae Today Lets 5% Down on Multifamily

It will set you back thousands of cash buying a keen average money spent. No matter if traders use a residential property financing to pay for 80-90% of your own cost, you to definitely still you will indicate discovering $fifty,000. To own an individual investment property.

Exactly what on the citizen funds, that funds 95%, 97%, even 100% of cost? Is real estate people ever fool around with homeowner fund buying local rental services?

In later 2023, Federal national mortgage association refurbished the rules to finance as much as 95% LTV getting multifamily features with doing four devices. The alteration applies to practical requests, no-cash-aside refinances, HomeReady, and you can HomeStyle Renovation funds.

Which means buyers is also set out just 5% on the duplexes, triplexes, and fourplexes, which have purchase pricing around $step 1,396,800. To meet brand new homeownership requirement, you ought to are now living in one of the equipment for around 1 year. Upcoming, you could get out and maintain the house since the a living assets.

Report about Fannie Mae’s HomeReady Loan Program

It will not should be their basic domestic, therefore doesn’t have to be a buy mortgage refinances are allowed.

Minimal credit rating to possess an excellent HomeReady mortgage loan was 620. That’s nicely reduced, however as little as FHA’s minimum credit ratings (580 to own an effective 3.5% down-payment, 500 having good ten% downpayment).

Let me reveal in which it will become a while gluey for real property dealers. To qualify for a good HomeReady possessions loan, Federal national mortgage association and Freddie Mac computer create enforce money restrictions in some components.

In several areas and you may residential property tracts, there are no debtor americash loans Oak Hill money ceilings. In others, they’ve been according to research by the geographic area average money (AMI). You can examine certain neighborhoods’ income ceilings to possess HomeReady finance here.

It’s some time unusual: You truly need to have adequate income to spend us straight back, but not more than nearby mediocre earnings! Of many homebuyers and home hackers find it a soft line so you’re able to walk.

Freddie Mac’s Domestic You are able to Loan System

Freddie Mac computer released a similar mortgage system named House You can. The applying provides one or two options for capital features: that having a good 5% down payment and one with an excellent step three% down payment.

Towards the step three% down solution, a positive change out of Fannie’s HomeReady system is that the lowest credit score is a bit highest at the 640. Nevertheless 5% off solution lets consumers without credit history a huge boon for many of us who have not yet based its borrowing from the bank.

On account of a few almost every other sweet advantages out of both Freddie Mac’s Family Possible and you may Fannie Mae’s HomeReady loan apps. First, they won’t wanted lifelong home loan insurance rates, as opposed to FHA’s new financing rules. Since the loan balance falls below 80% of the property value, individuals normally query the bank to eliminate the borrowed funds insurance rates.